Top 10 Things 2025 Tax Changes Every Single-Owner LLC Should Know

by Adam C. Bell, CPA

As we head into the 2025 tax year (for returns filed in 2026), Congress has enacted major changes under the One Big Beautiful Bill Act (P.L. 119-21, also “OBBB” or “OBBBA”) that impact everything from standard deductions to how pass-through business income is taxed. If you operate a single-owner LLC (whether a disregarded entity on Schedule C or having elected to be taxed as an S Corporation or C Corporation), these are the top 10 changes or reminders you’ll want to know. Getting ahead of these can affect your tax planning, estimated payments, and financial strategy.

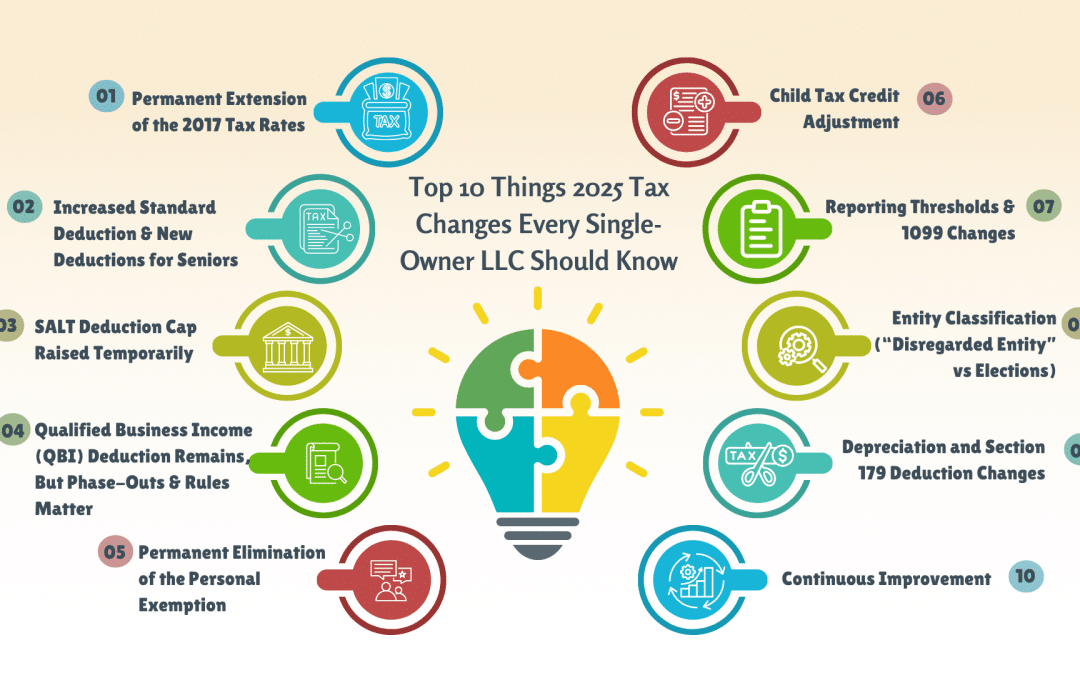

1. Permanent Extension of the 2017 Tax Rates

- The 7 individual tax-brackets established under the Tax Cuts and Jobs Act (TCJA) are now made permanent. That means the familiar rates (10%, 12%, 22%, 24%, 32%, 35%, 37%) will continue for 2025. (U.S. Bank)

- For single-owner LLCs taxed via the owner’s personal return, this stabilizes your marginal rate expectations. If you expected rates to revert, that’s no longer the case. Adjust your projections accordingly.

2. Increased Standard Deduction & New Deductions for Seniors

- The standard deduction has been increased for all filing statuses. For example, single filers and married individuals filing separately receive a higher standard deduction. (U.S. Bank)

- There’s an additional temporary “bonus” deduction for older taxpayers (65+), which can stack on top of the regular standard deduction. (Kiplinger)

- For business owners, this can shift whether you itemize or use the standard deduction, and thus affect your net taxable income (especially if your LLC’s deductions are modest or your filing status/senior status changes).

3. SALT Deduction Cap Raised Temporarily

- One of the major changes is that the state and local tax (SALT) deduction cap is increased from $10,000 to $40,000 (for individuals) for 2025–2029. (Wikipedia)

- There are income phase-outs: for those with high modified adjusted gross incomes (MAGI), the benefit begins to reduce. (Wikipedia)

- If your LLC is in a high-tax state, this could make a material difference. Revisit whether itemizing SALT and other deductions becomes beneficial again.

4. Qualified Business Income (QBI) Deduction Remains, But Phase-Outs & Rules Matter

- The 20% Qualified Business Income deduction for pass-through entities (sole proprietorships, single-member LLCs, etc.) is still available. (wierenga.tax)

- Be mindful of the taxable income thresholds. When your income is above certain levels, the deduction phases out or is restricted (based on type of business, W-2 wages, etc.). It remains critical to model whether investment in wages or property can help maximize QBI benefits.

5. Permanent Elimination of the Personal Exemption

- The personal and dependent exemptions remain eliminated, as they had been since the TCJA. (Kiplinger)

- While it’s not new, it’s now further cemented, so you should not expect those to return under current law. This affects your total deductions especially if you have many dependents.

6. Child Tax Credit Adjustment

- The maximum Child Tax Credit (CTC) is increased from $2,000 to $2,200 per qualifying child for 2025. (Wikipedia) · The credit and its refundable portion are indexed for inflation going forward. (Tax Foundation)

- Single-owner LLCs with families should update their expected CTC when preparing returns and planning cash flow.

7. Reporting Thresholds & 1099 Changes

- Some reporting thresholds for Forms like 1099-K are affected. For example, thresholds for using Form 1099-MISC and 1099-NEC are being adjusted (notably, the minimum amount one must receive before the IRS requires the reporting entity to issue a 1099). (Wikipedia)

- Ensure your bookkeeping captures the correct thresholds so you don’t run afoul of missed reporting.

8. Entity Classification (“Disregarded Entity” vs Elections)

- If you are a single-owner LLC and haven’t elected to be taxed as a corporation, you remain treated by default as a disregarded entity your LLC’s income and expenses flow through to your individual return. (IRS)

- If you have made, or are considering, an Entity Classification Election (via IRS Form 8832 or Form 2553 if S-Corp), double-check that your anticipated profits, self-employment tax, and payroll obligations still make that election favorable under the new law.

9. Depreciation and Section 179 Deduction Changes

- Under the new law, Section 179 deduction limits are higher, and the phase-out threshold is extended. For many LLC owners investing in equipment, machinery, or other qualifying property, this can allow more upfront write-offs. (wierenga.tax)

- The ability to fully expense certain property (bonus depreciation) and how “qualified depreciable property” is treated has also been clarified or made more favorable in some instances. (Proskauer Tax Talks)

10. Tax Planning & Estimated Payments

- With many changes to credits, deductions, and thresholds, your tax liability may change materially from previous years even with similar revenue. Guard against surprises by updating your projections.

- Adjust estimated tax payments accordingly, especially if your income is rising (or falling), or if you anticipate moving into a different tax bracket, losing or gaining deductions or credits (e.g., due to new itemization options, or SALT cap changes).

- Also, consider how your business structure (disregarded entity vs S-Corp vs C-Corp) may affect self-employment taxes, payroll withholdings, and other tax obligations.

Practical Takeaways / What to Do Now

- Run the numbers: Use your 2024 data to simulate your 2025 return under both “old rules vs new rules” paths, especially for deductions, SALT, and QBI.

- Reassess entity election: If you’ve been taxed as an S-Corp or planning to, make sure that decision still makes sense in light of changed deductions, credits, and reporting burdens.

- Keep detailed records of expenses, especially those that affect key thresholds (e.g. wages, property placed in service, business use, etc.).

- Adjust withholding & estimated payments so you avoid underpayment penalties.

- Engage a tax professional: These laws have many moving parts. Small differences (e.g. a little more SALT, a bit more income) can change what’s optimal for you.

Conclusion

The 2025 tax year brings several welcome clarifications and enhancements for single‐owner LLCs, especially around permanent tax rates, increased standard deductions, and more generous depreciation/Section 179 write-offs. But with those upgrades come complexity, particularly around thresholds, phase-outs, and reporting changes. Being proactive running your own projections, keeping good records, and possibly consulting your CPA can help you maximize the benefits and avoid surprises.

Ready to take your business further? Let’s connect at staging-acb-logistics.devsquad.tech

Sources Cited

- IRS: Single Member LLCs – classification and treatment. (IRS)

- IRS: One Big Beautiful Bill Provisions. (IRS)

- Tax policy, Tax Foundation, etc.: FAQ on OBBB. (Tax Foundation)

- Kiplinger / US Bank overviews of standard deduction, tax brackets. (U.S. Bank)

- Proskauer analysis: depreciation and qualified property changes. (Proskauer Tax Talks)

The information provided in this article is for educational purposes only and is not intended as, and should not be relied on for, tax, legal, or accounting advice. Laws change and may vary by jurisdiction. You should consult your own tax, legal, and accounting professionals before making any decisions. No professional–client relationship is created by reading this content.